MCA Update: ‘MSME Form I’ Filing by Specified Companies

Also Read: Benefits of MSME Registration in India

Introduction:

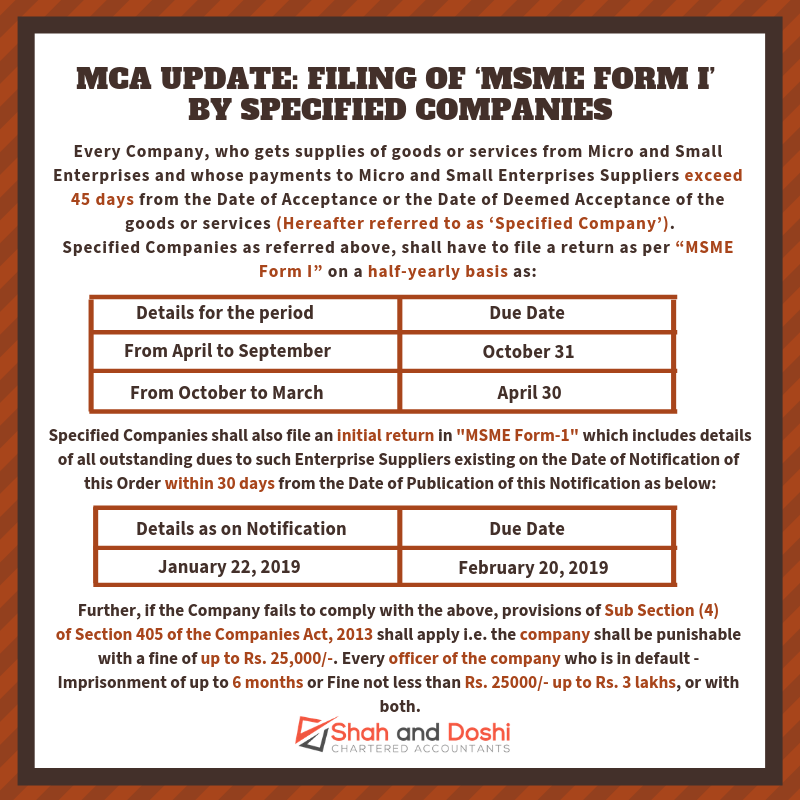

Ministry of Corporate Affairs (MCA) vide notification number S.O. 5622(E), dated the 2nd November 2018 has directed that Every Company, whether public or private or OPC who gets supplies of goods or services from Micro and Small Enterprises and whose payments to Micro and Small Enterprises Suppliers exceed 45 days from the Date of Acceptance* or the Date of Deemed Acceptance** of the goods or services (Hereafter referred to as ‘Specified Company’) shall submit a half yearly return to the MCA in “MSME Form I” stating the following:

(a) The amount of payment due; and

(b) The reasons for the delay;

Specified Companies as referred above, shall also have to File an initial return in “MSME Form I” which includes Details of all outstanding dues to such Enterprises Suppliers (hereafter referred to as “Specified Dues”) existing on the Date of Notification of this Order within 30 days from the Date of Publication of this Notification i.e. 20th February, 2019.

* “The Day of Acceptance” Means,-

(a) The day of the actual delivery of goods or the rendering of services; or

(b) where any objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day on which· such objection is removed by the supplier;

** “The Day of Deemed Acceptance” Means,-

where no objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services;

Types & Due Dates of Return:

| Details as on Notification | Due Date | Information required to be submitted with ROC |

|---|---|---|

| Initial Return / One-time Return From January 22, 2019 | February 20, 2019 | - Total amount outstanding to all MSEs as on 22.01.2019 - Details of Financial Year, Name and PAN of supplier, amount due and date from which amount is due - Reasons for delay in payments due |

| Half-yearly Return From April to September | October 31 | - Total Amount outstanding to all MSEs during April to September and October to March respectively - Details of Financial Year, Name and PAN of supplier, amount due and date from which amount is due - Reasons for delay in payments due |

| Half-yearly Return From October to March | April 30 |

Consequences on Default:

Further, if the Company fails to comply with the above, provisions of Sub Section (4) of Section 405 of Companies Act, 2013 shall apply.

If any company fails to file MSME Form-1 or knowingly furnishes any information or statistics which is incorrect or incomplete in any material respect:

- The company shall be punishable with fine which may extend to Rs. 25,000/- and

- Every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000/- but which may extend to Rs. 3 lakhs, or with both.

Micro, Small and Medium Enterprise as per Micro, Small and Medium Enterprises Development Act, 2006:

The Government of India has enacted the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 in terms of which the definition of micro, small and medium enterprises is as under Enterprises engaged in the manufacture or production, processing, services or preservation of goods as specified below:

| Enterprise Type | Sector | |

|---|---|---|

| Manufacturing (Investment in plant & machinery) | Service (Investment in equipments) |

|

| A Micro Enterprise | Does not exceed Rs. 25 Lakhs | Does not exceed Rs. 10 Lakhs |

| A Small Enterprise | More than Rs. 25 Lakhs but does not exceed Rs. 5 Crores | More than Rs. 10 Lakhs but does not exceed Rs. 2 Crores |

| A Medium Enterprise | More than Rs. 5 Crores but does not exceed Rs. 10 Crores | More than Rs. 2 Crores but does not exceed Rs. 5 Crores |

Note: Medium Enterprises are not covered for the purpose of MSME FORM I.